Yes, You Can Find Vintage in River North: 55 W. Erie

Amidst the high rises that dominate the River North neighborhood, there are still remnants of the area’s past including 55 W. Erie, a 9-unit brick vintage building.

This 2-bedroom top floor unit has been completed rehabbed but this is no cookie-cutter rehab.

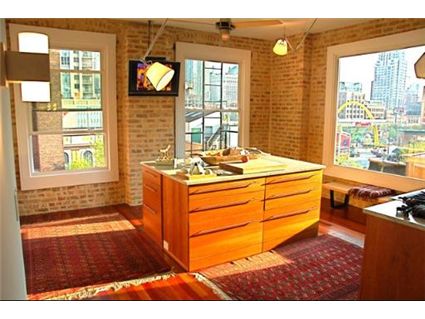

The kitchen, which is a massive 26×13, has an oversized stone island, a Wolf range and a Subzero glass front refrigerator.

The unit also has 2 fireplaces, including one in the master bedroom.

There’s central air and an in-unit washer/dryer but there’s no parking (although it’s available for rent in the neighborhood.)

Elizabeth August at @Properties has the listing. See all of the pictures and a virtual tour here.

Unit #4W: 2 bedrooms, 1.5 baths, 1700 square feet

- Sold in August 2003 for $335,000

- Originally listed in April 2009 for $524,900

- Reduced

- Currently listed for $499,900

- Assessments of $414 a month

- Taxes of $3726

- Central Air

- In-unit Washer/Dryer

- No parking

I clicked the link but couldn’t take my eyes off the photo of the Realtor.

Shows very well and unique. However, the lack of full 2nd bath and no parking is a killer. No way I would pay $500k. Someone might, but most of the people who are going to have the means to buy this place are going to want the 2nd bath and at least one space.

Many mortgage insurance companies are not insuring building with less than 10 units right now. This looks like an 8 unit building. The buyer will likely need 20% down or FHA with a large enough down payment to get the loan to $410k in most cases.

are stainless steel fridges on the way out? maybe I should start a biz swapping out stainless doors for glass.

Nice place. Berber carpet on bathroom wall is interesting.

Good call AMW! I love the LeCorbosier pony chaise in the living room too… I wonder if its real or a knock off. Looks like a strange layout, i’d like to see a floor plan.

BABE!

> Many mortgage insurance companies are not insuring building with less than 10 units right now.

I don’t understand why this is. Are people less likely to pay their mortgage on a smaller building? I think it would be the opposite, since every place I have looked at with more than 10 units, had like 50% of the units for sale at once.

Sabrina should add a Realtor Hot or Not section…

Brad:

It is because if an owner defaults in a smaller building, the other owners are going to have to pick up a larger share of the up keep. Chicago is a unique market in that most of our condos are in smaller walk ups and like you said, people generally woujldn’t touch a larger development.

However, I think nationwide, smaller developments are riskier. the MI companies are applying nationwide stats and underwriting guidelines to a local market. It doesn’t make sense in Chicago, but this is what happens when you have statisticians, accountants, and MBA making decisions purely on excel models instead of front line knowledge.

Russ, I agree!

#

Russ on June 11th, 2009 at 10:38 am

Sabrina should add a Realtor Hot or Not section…

Hmmm, I have an idea….

really lovely unit, but walking four flights of stairs isn’t good for anyone except peapod. great view of golden arches.

No parking, not even two full baths, and no, the realtor is not that hot. Also the layout of the kitchen doesn’t make sense to me.

380k for this one. Next.

Nice unit but the walk up, lack of parking is a deterent. Also, the building directly to the left (east) of this one houses the Joynt, a cheesy “retro” nightclub.

the unit/building is very cool. I could live without all of the lamps on the walls.

Russ / A – Shall we start a new blog? 😉

Says parking is garaged/leased whatever that means.

Lovely unit.

Used to walk by this place all the time during my lunch hour. Price doesn’t seem out of line with current wishing prices in River North … but still overpriced. Especially without parking in that neighborhood.

“Many mortgage insurance companies are not insuring building with less than 10 units right now. This looks like an 8 unit building. The buyer will likely need 20% down or FHA with a large enough down payment to get the loan to $410k in most cases.”

It is rediculous on this site how many people think it is ok for someone to put down 3.5% or 5% or something like that. Mortgage companies shouldn’t give out loans unless you can put down 20%. If you don’t make a big enough salary in your job to afford the 20% downpayemnt, then the fact of the matter is that the place you are looking at is out of your price range, so start looking at something cheaper. People who put down less than 5% helped get the housing market into this mess. I am all for the banks, lenders, etc. requiring 20% down or there is no deal. That is how is should be ALWAYS. If you are looking at a $500K condo, and you can only afford to put down 25K, well that is absolutely absurd. Start looking at something less expensive.

Disappointingly modern interior.

> I am all for the banks, lenders, etc. requiring 20% down or there is no deal.

That means less business for the banks. Banks like more business so they can make more money. A government regulation would be required for this to happen.

“If you don’t make a big enough salary in your job to afford the 20% downpayemnt, then the fact of the matter is that the place you are looking at is out of your price range, so start looking at something cheaper.”

You are probably right, but as long as the govt keeps encouraging this stuff, why not take advantage of it? I personally have the means to put 20% down on all the places I am looking at. Will I put 20% down? Probably not, unless the place is too expensive to get an FHA loan.

Why would I tie up capital that I don’t have to? Why would I throw a significant sum of money at an asset that is likely to decline in value in the near-term? Moral hazard? Of course. But hey, I didn’t sign off on these idiotic rules…I am just going to try to take advantage of them.

Perhaps I’m just tickled that the kitchen has walls separating it and the other living spaces, but I really like that kitchen. I know my friends and family tend to gather and drink/pick-at around the kitchen when we are together and many of these open kitchens tend to take away some of the kitchen gestalt.

That said, no deeded parking ruins it for me. That and, while it may be amusing at times, watching the drunks stumble for late night snacks at McDonalds and then shout to the heavens when they realize there isn’t a dollar menu may get old quick.

Exactly, who wants to lock up all that capital in an illiquid, slowly appreciating or even depreciating asset, when you can get a better rate of return elsewhere?

Bobbo,

I completely agree. Unfortunately the way it should be and the way it is are two different animals altogether. However you are correct in that our government is currently acting in a manner to the long-term detriment of its citizens and in a wholly inconsistent manner.

Our policy makers created the bubble via slowly lowering the percent downpayment on mortgage loans. In fact even when the FHA was first created you needed 20% down. Their current efforts seem more geared towards trying to keep the shaky house of cards propped up by the bubble as opposed to making sure this never happens again.

The only way to try to keep the shaky house of ponzi economics (aka rising RE valuations) from coming apart is to lower the barriers to entry _even more_ in an attempt to entice even more into real estate ownership. Look at the 15k credit they are talking about now.

Allowing people with no or minimal downpayment opens the floodgates to allow many more people to buy overpriced real estate, with no incentive to not default if their speculation does not pan out. This is one prong of the government’s plan to stabilize the housing market. The other is inflation.

Its going to be a rough few years of W shaped bottoms until the policies are put in place to prevent those who don’t belong in the home ownership (aka RE speculation) game from doing so cannot.

Basically the people’s paradigm towards RE is going to have to change from one of entitlement to a privilege. And it seems Americans have an increasing entitlement paradigm with each passing year so this might take awhile to change.

For instance no college graduate in their 20s (especially most who are saddled with student loan debt) is entitled to own a condo. I’m not sure where that entitlement came from but it definitely needs to change.

“Why would I tie up capital that I don’t have to? Why would I throw a significant sum of money at an asset that is likely to decline in value in the near-term?

Because you like it and the neighborhood and you want to live there and the gain is in the enjoyment of having a really need place in a great location?

“Neat”

Steve A,

MJ can attain all of the things you mentioned without putting his capital at risk. Instead he can put our (taxpayer) capital at risk. If valuations continue to tank over the next few years he can walk away leaving us with the loss.

His behavior is entirely rational. Its our government’s policies that are completely irrational.

Bob, what is this 15% credit you speak of?

The problem is current valuations are based on much looser financing. It was one thing to require 20% down when you could actually buy a decent place for under $200k. However, requiring that sized down payment would absolutely destroy current values. Given that 60% or so of the country owns homes, it would be disaster for the economy if a large chunk of those people were saddled with such a huge devalued asset. You think it is bad now, wait until you absolutely cannot get a mortgage without 20% down.

Low down payments by themselves are not necessarily bad. It was low down payments to borrowers with marginal credit, income, and investors/speculators where banks shot themselves in the foot. Of course, Wall Street was buying the paper, but any mortgage broker with a GED could have told all the Ivy League guys at on the Street the paper was garbage. It is one thing to allow a new professional grad making $100k+ to buy his first home with 5% down vs Joe Six Pack with a 630 FICO and 30 hours a week at Jewel. That line got blurred by the banks…

There is talk on the hill of expanding the first-time home buyer credit, currently at 8k and restricted to first-time purchasers who earn 75k or less, to 15k and removing all restrictions.

Its almost a large enough sum for me to buy a 150k place (the tax credit is 10% of the purchase price), then promptly default and live for free while the foreclosure proceedings are underway.

“It is one thing to allow a new professional grad making $100k+ to buy his first home with 5% down vs Joe Six Pack with a 630 FICO and 30 hours a week at Jewel. ”

I can tell you there are probably going to be a lot of $100k+ professionals who bought places with 5% down who are at risk of losing their income stream.

Guess what happens to the bank in the foreclosure process when a homeowner has minimal skin in the game? Massive losses.

No living room is complete without a flayed animal carcass on the floor.

Btw, I am staunchly opposed to all the current policies that are meant to support the housing market and encourage home ownership. A year ago I would have never considered this based on principle alone. But the problem is that the “responsible” people are going to be the ones that are the most penalized by all of this. They will pay higher taxes, they will continue to bail everyone else out, and they will receive nothing. At the end of the day, I know I will be paying for these policies whether I participate or not. So why not participate?

“Berber carpet on bathroom wall is interesting”

HaHa.

Assuming that the current owners did all the visibile updating (i.e., kitchen, baths–ioncluding the expensive wall o’ tile, crazy lamps, etc.), what do you think they have into it? $425K?

Gonna rock that 1br in uptown afterall eh bob? 8)

“Gonna rock that 1br in uptown afterall eh bob? ”

Just might! At my housewarming party people will be directed to please place their narcotics and weapons in the bin at the entryway. 8)

“people will be directed to please place their narcotics and weapons in the bin at the entryway”

So, you want the homeless to hang out hoping you have another party?

I can see the flyers now “bob’s 15 thousand dollar crack party, leave your guns at the door!”

And oh, this property backs up against the Portillo’s drive thru. Knock off 50k for that!

Bob:

Foreclosures are caused by loss of income – not down payment.

In fact, banks are lot less likely to foreclose if you have less equity. Who do you think they are more likely to work with, the borrower who only has 5% equity and is heading into default or the borrower who has 60% equity? They know they can foreclose on the guy with equity and minimize the loss. The 5% guy they are going to work night and day to ensure he keeps making payments. Downpayments are designed to protect the bank, not the borrower.

I would rather be a 5% down homeowner with $50k in cash for an emergency than a 20% down borrower with no cash left because I sunk it all into the house. Who do you think is going to go into foreclosure first if they lose a job?

“I can see the flyers now “bob’s 15 thousand dollar crack party, leave your guns at the door!””

Did you ever see the Chapelle skit when they entrusted their house to Tyrone Biggums and went on vacation? That would be my party.

Russ,

You are correct. However banks aren’t that stupid (close). I think for any kind of LTV above 80% they require PMI. So they would be pretty indifferent to foreclosure so long as the fair market value of the property is not less than 80% of the amount of the mortgage.

Bob:

Yes, but your forget most of these loans are piggyback mortgages with no PMI. Also, PMI companies are not necessarily playing nice with the banks claiming the banks knowing made bad loans. Look for the lawsuits against banks for unwarranted PMI claims.

The point is just that low down payments not necessarily bad. The risk layering has to make sense. Banks let things get too loose and now they have over tightened, making things worse. Things will settle to a happy medium. I don’t advocate 100% financing, but I also don’t think requiring 20% down is realistic or prudent for most home buyers in today’s world either.

For those of you wondering what the new $15k tax credit is all about that Bob was talking about. Here is an article about bill that was proposed and sponsored by many senators today.

http://www.bloomberg.com/apps/news?pid=20601213&sid=aI3l8W6tflrg

Russ / All:

If someone were to get an FHA loan (capped out at $410k) and paid $500k for this place… do they have to fill that whole with $90k of equity, or can you get a second mortgage to fill a portion (up to 90%/$450k) for example?

In the same sort of example, what have folks seen recently for second mortgages behind $417k conforming loans (do they still exist? through what % of purchase price will they lend to?)

Thanks!

BoA told me a few weeks ago that second mortgages no longer exist. Has anyone heard anything different?

I can’t tell you if they are gone today but one was used by the purchaser of 3816 N Fremont in April (featured in next post.)

Puchased 4/3/09 $700,000 with 85% total financing:

mortgage with MERS $417,000

mortgage with Midwest B&T $178,000

Since this apartment has been bashed enough, I think I will take a different route and bash the interior decoration…or at least correct some previous comments.

That is not Berber carpet on the bath wall. I cannot remember the name of the upscale wall/window covering company right now. I know they are based in NYC and have been featured in Chicago’s LUXE design mag. They offer many heavily textured ‘green’ coverings of this type. My fav is their woven bamboo design that has a bread basket like design. Very ‘now’ in decorating and very expensive as well.

The LeCorbusier lounge is a replica and the fabric is actually microsuede made to look like a real skin. Same with the ‘animal carcass’ on the floor.

While I am a huge fan of unique lighting, they really went overboard in the kitchen. Just from the limited pics, I see four different styles. Way too many even at that size and they don’t have any common design factors. Same with lighting in LR…butt ugly and it ended up being a focal point…if you can draw your eye away from that fireplace with two types of brick on the same surface.

Hardwoods and rugs in the kitchen? Come on now. I am assuming there is a wall of cabinets somewhere out of camera range? Love modern but not impractical modern. Cooktop is right next to the fridge. NO. Love the glass ref door, but am bothered by no window coverings on those huge kitchen windows. Day and night both, it is not a wise decision to go without window coverings…those floors will be sundamaged in a few years. I graze standing naked with the frige door open at 3 AM, but I guess not in this kitchen.

With that much natural light I would do some bold colors, esp with all that brick. White just does not go.

OK I am done…next?

Walk up four floors? NO No parking in RN? Where would you park your R8?

dogowner,

If you have to ask, you obviously can’t afford a 500k place.

Why not try saving up money instead for the property of your dreams instead of borrowing yourself into oblivion?

Harsh Bob, Harsh!

Dogowner:

The second mortgage/Heloc market is pretty much dead. Most 2nd lenders won’t go above 80% combined loan to value. You also cannot get PMI on loans above $417k in Chicago. This is why the $500k+ 2/2 condos are just sitting on the market. The folks the can afford the payments on them don’t want to come up with the down payments required to keep the loans at $417k OR can’t get second mortgages to break up the loan.

All of the DINK (Dual Income, No Kids) buyers right now are buying properties where they can put 10% down and still get a $417k ($463k max purchase price) loan OR do 20% down and get a $417k mortgage ($521k max purchase price).

Sutff priced above %525k really isn’t moving from what I am seeing or it gets negotiated way down.

Editor’s Note:

Once again- I remind all of you (especially those of you who are “new” to the site) that the interior decoration is meaningless (as far as furniture, paint colors etc.)

Colors and light fixtures can be changed by the new owner. The furniture will not be there when you move in.

This isn’t a site about interior decoration. You can go to Apartment Therapy or those sites for that.

However, discussing a kitchen or a bathroom renovation and/or features is more fair game.

Please keep it on topic to the property and real estate. Thanks.

“And oh, this property backs up against the Portillo’s drive thru. Knock off 50k for that!”

This is incorrect. This building does not back up to the Portillo’s. It’s not even on the same block.

Thanks for the good mortgage info Russ. Very interesting.

I’m also seeing the $550k to $650k market being pretty dead.

But I AM seeing some movement in the over $700k properties ($700k to $850k or so.)

According to G- that Fremont purchaser used two loans and only 15% down- so possibly lenders are being a little more lenient on the higher end???

Sabrina:

They are pretty much gone. A few banks were going to 85 CLTV a few months ago, but most have curtailed them. I will have to check if B&T is still doing them. A few will do it on single family homes, but not condos.

Usually the buyers in the $700+ range can swing the down payments required to get decent jumbo rates, so that market is moving unless the buyers also need to sell.

Unless financing loosens up a little bit, I don’t think there are going to be many 2/2 above $450k except in a handful of true luxury buildings. The days of the late 20s/early 30s Chads & Trixie’s buying the 2/2’s in Lincoln Park for $500k are done.

you actually need 25% downpayment for condo’s in chicago now to avoid fees/pmi due to knew freddie/fannie rules, right??…or maybe i misunderstood my lender.

^knew=new (hoping i dont get roasted for my type, tough crowd around these parts!)

You need 25% down on condos to avoid risk based price adjustments that Fannie/Freddie charge. The fee is .75% of the loan which typically translates into about .25% in the final rate. In other words, if you have a $400k loan on a condo and didn’t put 25% down, Fannie/Freddie charge banks $3,000.

You can either pay that as an origination fee (points) to the bank or if they just roll it into the interest rate, it typically means your rate is about .25-.375% higher than the rate you would have been quoted had you bought a townhome or a single family home.

This is a nice building, but I still do not know how can people pay so much for rent and purchase, see news today about one woman wants to jump out of the building, let’s all hope that she is not going to do it.

Chicago Realtor, i sincerely hope you are not native to the United States.

Why? His/her English is not much worse than that of many other Americans…

Not only is this property located very near a couple of 4 AM closing nightclubs (Joynt and Excalibur) but is also one building away from the Dearborn/Erie intersection.

This intersection is on the main Northbound route for the fire station that is located a few blocks south. For some reason, the fire engines really likes to lean on their horns at this intersection.

So, late night clubs (with lines) and lots of Northside fire calls will give the new owner a real “city feel”.

Hi Sonies, I was not, sorry about my English, but actually I thought I was posting on the list of 340 Randolph, that’s why I posted that comment.