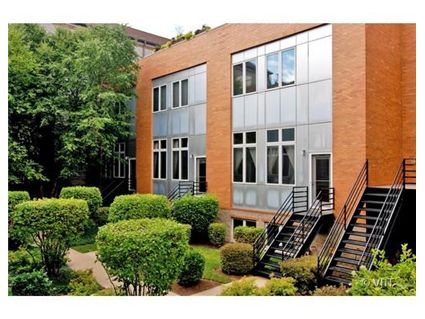

Getting More Space in a Townhouse: 1742 N. Winnebago in Bucktown

This 3-bedroom townhouse at 1742 N. Winnebago in Bucktown has more square footage than most single family homes at a similar price point in the neighborhood.

Built in the mid-1990s, it also has the open concept floorplan that is missing in most of the vintage homes nearby.

At 2934 square feet, the townhouse has 11-foot ceilings, stainless steel appliances and granite countertops in the kitchen and a large family room with custom cherry built-ins.

It also has all 3 bedrooms on the same level and a 2-car garage.

As an added bonus, for those summer months, the townhouse has a roofdeck with built-in bar.

Is this townhouse a good alternative to the Bucktown single family home?

Robert John Anderson at Baird & Warner has the listing. See more pictures here.

Unit #B: 3 bedrooms, 2.5 baths, 2 car garage, 2934 square feet

- Sold in November 1996 for $304,500

- Sold in April 2004 for $542,500

- Sold in January 2006 for $611,500

- Sold in April 2007 for $662,000

- Originally listed in August 2009 for $649,000

- Reduced

- Currently listed for $635,000

- Assessments of $55 a month

- Taxes of $7,040

- Central Air

It’ll sell in the low $500k’s

Is it just me or does anyone else think it is weird to have painted the original wood trim white but leave the windows natural wood? It seems people are anti natural wood trim these days, but a lot of 1990’s units used this throughout. Personally, it doesnt bother me to have natural wood trim but the halfway approach definitely does not work. All white or all wood. Make up your mind.

how loud is the blue line here? the map makes it look like it’s right across the street from the property…

I hope whoever gets this place likes listening to the Blue Line…

Damn, they sure loved tubular steel in the 90’s, didn’t they?

I’d almost rather have the barn.

I think the $55 monthly assessment will be the killer here…

Call me crazy, but I actually like the exterior.

The comment about the assessment is a joke, right? That barely covers the cost of lawn care.

The mortgage calculator at the right hand side of the page of the Baird & Warner link estimates that with a 30 year fixed mortgage the estimated monthly payment is $3,953 with a required income of $144k – using an asking price of $635,000 with a down payment of 20.0% and a loan amount of $508,000.

$4,000 a month…is a little pricey even for my lawyerly income. However, according to the link (by clicking on the 5/1) if I use a 5/1 Interest Only ARM my monthly payment is reduced to *only* $2,700! Where can I sign up for that deal? That’s what I want. I’ll just live here for five year and then either refinance or sell for PROFIT!

(yes I know there are interest rate assumptions, etc, but I’m just repeating what Baird & Warner is telling me and they’re obviously pushing me into the 5/1 IO ARM because the payment is way cheaper)..

“with a 30 year fixed mortgage the estimated monthly payment is $3,953 with a required income of $144k – using an asking price of $635,000 with a down payment of 20.0% and a loan amount of $508,000.”

And that’s presuming the bank will give the buyer a jumbo at the stated rate.

Click thru and play around with their full caclulator and the difference b/t a $417k mtg (conforming) and a $417,001 mtg (jumbo) is $365/month. That’s a big difference.

If you paid $521,250 and put down 20% (to get to the $417 magic number), the calc shows $2995/month–which doesn’t seem too bad for a place this size.

$521k is $114k or 18% lower than the current asking price. That’s asking a lot from this owner. I couldn’t determine the financing with CCRD, but, I doubt most owners would willingly sell for that low except in a short sale situation. $521 puts this into the 2001-2003 price range…I think the el is a huge issue for this place, I see this as a high $400’s, tops, but it’s headed into the low $400’s. It’s a townhouse in bucktown for goodness sakes. Where I grew up (a half an hour drive w/ light traffic) townhomes were for the lower-middle class folk who couldn’t afford a ‘real’ house. Granted they weren’t 3,000 sq ft like this one but still, it’s a townhouse.

“$521k is $114k or 18% lower than the current asking price. That’s asking a lot from this owner.”

Well, yeah, but that’s the price that makes it somewhat reasonable to buy, in my view. The 2004 price seems about right, and would probably be close enough to make it possible for someone who has $104k to spend on a DP to somehow make it work.

“townhomes were for the lower-middle class folk who couldn’t afford a ‘real’ house. Granted they weren’t 3,000 sq ft like this one but still, it’s a townhouse.”

But that’s all about the 3 Ls of real estate. Go to other large cities of the world (which have more in common, housing-stock-wise, with central Chicago than greater-Schaumburg does) and townhouses are basically the top end. So that’s a locational thing. But you know that.

Location = bucktown. structure = townhome. $635k = FAIL.

“$4,000 a month…is a little pricey even for my lawyerly income”

But if you had Mr.Mrs. HD, then $4k ain’t so bad.

HD, what is your lawyerly income anyway?

I’m sure HD’s income is enough for Obama to claim “that he’s doing okay”

“Location = bucktown. structure = townhome. $635k = FAIL.”

But its a reeeealy reeeeeealy big townhome, and things are different in Bucktown now don’t you know?

There’s a disconnect between listing prices and transaction prices, at least if Case Shiller is to be believed. Case Shiller is at something like 2003 prices. Few if any listings are within 5 percent of 2003 prices. So properties sit for a long time.

Now, owners will look at Case Shiller trending slightly up, say there’s a bottom, and choose to keep list prices as they are, ignoring the fact that most sales are at levels far lower than they would take. And everything continues to sit out there. I can wait this out, but I would prefer not to.

I’ll be honest here because I don’t really care, I’m not an internet millionaire, I’m doing just fine and so is Mrs. HD. The partners you read about in the newspapers earning in the $300’s, $400’s, $500’s, that doesn’t happen until your 40’s or 50’s, or if you’re extraordinarily lucky, in your 30’s. I’m not quite there.

I’m not working in biglaw, nor am I working small law, so I’m somewhere in between. And that’s not really any surprise given what I’ve discussed on here. I pay my bills, I pay my rent, I pay the student loans, and I’ve got a decent chunk of money left over every month which sits in the bank (and because of deflation is becoming more valuable every day) until this housing mess gets sorted out.

Regardless of what I earn, $4,000 a month is a significant amount of money for housing. Which is sort of the problem, is that people who earn what I earn don’t think that $4,000 is a lot for housing, even though they are often stretched financially to make the payment (after the car payment, tuition, credit cards and student loans), and quite a few people earning less than me think $4,000 is perfectly acceptable.

Unfortunately, sellers who are paying $4,000 a month still think it’s OK to pay that much, but the reality is that there aren’t enough buyers willing or able to take on that kind of monthly mortgage obligation. Yes there are people who can afford $4,000 a month, there are plenty of them, but there are plenty more units available for $4,000 a month than there are takers…the market is really distorted…

“AK49 on September 30th, 2009 at 12:41 pm

I’m sure HD’s income is enough for Obama to claim “that he’s doing okay””

Did someone say Bucktown? 🙂

nice place, sweet size, 2 car parking!!!

right on the tracks 🙁 but in between stops 🙂 and to add what DZ maybe implying its above the 2004 price? and its still a townhome with shared walls.

Inbetween stops = really ****ing loud noises every 20 minutes.

If you want to get slightly farther away from the tracks, you can try the townhouses on the other side of the tracks/Milwaukee at Churchill/Leavitt. There’s a bunch listing over $700K.

Sounds like a Bucktown home of genius to me

“Inbetween stops = really ****ing loud noises every 20 minutes”

trying to put a positive spin… like realtor should list “a roof top deck were you see new friends everyday”

“$4,000 a month is a significant amount of money for housing”

It is, but using “traditional” metrics, at 28% of gross, it’s “appropriate” for a household income of $171,428.

Are there more $635k condos and houses in Chicago than there are $171k-earning households? I would bet there are. Which is not a good thing for anyone trying to sell any property for $635k or more, as it leaves those who can easily afford it with too many alternatives.

also that really loud noise every twenty min is only for 10 seconds, more positive spin.

“Are there more $635k condos and houses in Chicago than there are $171k-earning households? I would bet there are. ”

Lets not forget the dual impact of fewer 171k households existing in this economic downturn than during boom times combined with the increased supply of 635k condos built during the boom.

This entire segment in the city of these 635k condos is toast in 90+% of neighborhoods, IMO. Gold Coast and River North might be the exceptions.

3 years from now $635k is going a really nice place; not gold coast mansion nice, but definitely sweeter than a 1990’s 3 bedroom townhome on the el tracks.

“3 years from now $635k is going a really nice place”

or a really crappy place… depending on what happens!

I hope my income goes up to compensate for the rise in prices or else we’ll all be poorer for it!

“Sonies on September 30th, 2009 at 2:01 pm

“3 years from now $635k is going a really nice place”

or a really crappy place… depending on what happens!

“

Don’t worry, Barack Obama will make certain that everyone will be making over $250k (through some hyperinflation) so he can raise taxes on them…

“I hope my income goes up to compensate for the rise in prices or else we’ll all be poorer for it!”

I won’t be poorer if you income doesn’t go up.

That’s the *real* point, tho–when does the decline in house prices get trumped by inflation (from $$ depreciation or otherwise) and decay of real incomes? It’s not *just* about buying at the right time w/r/t the bottom for real housing prices; you need to watch out for income erosion and other inflation/interest effects.

Unless your a deflation true beleiver, but then you’ve got a pretty long horizon for actually buying.

homedelete, can someone kindly explain why all the loan interest rate resets are so bad? Why would the 5/1 arm be bad?

Haven’t we been in a 30 year bond bull run, and aren’t interest rates going lower (as in Japan-style) if this deflation plays out the way Mish Shedlock says?

I keep hearing about resets, but shouldn’t they be a non-factor given rate drops in the US?

I took Sonies “depending on what happens!” comment to mean inflation in general, not just in housing prices, because the feds have been running the printing presses like crazy. If everything from energy to food to gas to building supplies to commodities costs more but our incomes are stay the same, that’s stagflation, and we’re all poorer because of it.

I think we’re looking at deflation for sometime forward, yes, but I’ll buy when it makes sense according to my income.

“I keep hearing about resets, but shouldn’t they be a non-factor given rate drops in the US?”

Mish also had a comment regarding your quite common misperception:

He said that lumping in Option ARM recasts in with ARM resets is akin to lumping dogs and cats together and treating all pet species as one.

Option ARM recasts are nothing like ARM resets. The vast majority of option ARMs payments will go up significantly at recast time as the loan switches from being a negative amortization loan to a fully amortizing loan at the accrued (increased) balance.

” If everything from energy to food to gas to building supplies to commodities costs more but our incomes are stay the same, that’s stagflation, and we’re all poorer because of it.”

General inflation does not necessarily lead to similarly inflated incomes and stagflation relates to growth (as in gdp) rather than incomes. Inflation, accompanied by growth or not, generally makes us generally poorer, tho (obviously) many will do well in a period of inflation–particularly those with income-producing assets which were highly leveraged before the onset of inflation.

I’ve repeated this ad nasuem but in short, in the example above, the difference between the PITI of a 30 year fixed and the 5/1 IO ARM is $1,300 a month, which basically means that in the case presented by Baird & Warner’s link, you can afford nearly 50% more payment with the IO ARM than the 30 year fixed. Which then drives up the cost of housing for everyone else who wants to buy with a 30 year fixed. 30 year fixed mortgage buyers get priced out because the of the guy who’s paying IO, and that distorts the pricing for everyone. Of course Ze will tell you that it’s better to save the money and invest it and do an arbitrage rather than sink your money into an illiquid asset, to which I respond that you’re repaying a contractual debt owed, not transferring to an illiquid asset. Regardless, Joe schmore making $117k a year gets to buy a house for a lower monthly payment than joe next door who needed $150k to qualify for the same house with a 30 year fixed. Before you know it a majority of those who buy in the upper end are using IO’s driving home prices higher and higher, and the sellers count on market appreciation (and innovative loan qualification standards) for equity rather than the good old time honored principal repayment. A few months back I showed a jumbo territory condo or house (i cannot remember) LP had something like 9 mortgages among 5 owners over the last 13 years and every one of them was an IO (and possibly ARM) loan. The 30 year fixed cannot compete with the IO pricing. It’s more leverage which drives up home values.

“homedelete, can someone kindly explain why all the loan interest rate resets are so bad? Why would the 5/1 arm be bad?

Haven’t we been in a 30 year bond bull run, and aren’t interest rates going lower (as in Japan-style) if this deflation plays out the way Mish Shedlock says?

I keep hearing about resets, but shouldn’t they be a non-factor given rate drops in the US?”

“Option ARM recasts are nothing like ARM resets.”

Oh, so it takes someone trying to sell you something to believe that? I should start up a GrowthEquityStablevalueAggressiveInternationalRussellIndexExplorerTripleLEverageBondRoulette Fund and try to market it with my pronouncements of the future, while 3 of the 5 funds my firm manages failed to react to the oh-so-obvious credit bubble until it was too late.

Mish is interesting and prolific, but so are dozens of others, and I don’t see where Mish’s actual track record reflects the accolades he receives.

I second Bob’s recast v. reset paradigm. Alt-A’s are in IL issue, I think there are 30 billion IIRC in the Chicago area, but I think the real issue is the Alt-A’s in the middle-upper income territory. Just because you can afford a $4,000 mortgage payment today does not mean you can afford a $4,000 mortgage payment next year. Ask anyone in the mortgage industry or big law or at an investment bank who was making hundreds of thousands a year and now makes significantly less. That’s where the problem lies. There are plenty of people who can afford the payment today but cannot afford the payment tomorrow. And when they decide to stop paying it will be a year and possibly longer before the REO goes on the market. Those properties are still working through the pipeline. There is a shadow inventory of 7 million foreclosures literally just sitting out there and that’s not counting the people who will default after that.

HD all IOs, by definition, have to be ARMs. Fixed rate is only possible for amortizing loans as its fixed for the life of the loan. As IOs never amortize, they can’t be fixed.

I meant to say option arms aren’t too big of an IL issue, only $30 billion, it’s the alt-a’s that are the issue.

“Mish is interesting and prolific, but so are dozens of others, and I don’t see where Mish’s actual track record reflects the accolades he receives.”

You did nothing to refute or even attempt to refute my point that option ARM recasts are nothing at all like ARM resets. The majority of the public and mainstream media sees recast and thinks/presents reset. The public then sees interest rates at historic lows (which are artificially created by the Fed these days and unsustainable) and believes there is no problem.

There is a huge problem with these option ARM recasts and we’re just at the beginning of the crapstorm.

I think we’re past that and with all the cash the banks have been making hand over fist with these low rates, the bottom of the real estate market has already happened, and Alt-a’s won’t have much of an effect as you think.

Most of the ‘shadow inventory’ will be sold to “buddies of bankers” and the rest of the garbage will be sold sometime down the road because the banks now have time on their side to let these non performing assets sit and collect dust until a greater fool comes along.

Only the big banks Sonies. Although the government is currently pushing to extend TARP access to troubled smaller banks. The Wells Fargo publicity disaster where a VP was caught using a multi-million dollar foreclosure as a weekend party pad while WFC was intentionally keeping it off the MLS lends credence to your theory.

We’re going to see the smaller banks drop like flies next year. Heck for the remainder of this year even. Its going to be a cold reality for many yokelville bankers who thought they could compete alongside the NYC hotshots (who pull the strings of government).

HD — the big law partners that do work for me all seem to clear $1,000,000 after associate profit, client credit and their own billing hours. It’s egregious, especially since their billing is rarely contingent or related to a successful outcome of their work, BUT that is a rant for another blog somewhere else.

What is true, and why I am making this point, is that the actual number of households that make over $500,000 in ordinary income is actually far fewer than you’d imagine. According to Claritas data, within the city limits of Chicago, some 5,500 families clear this benchmark. This excludes capital gains, but you get the point. Lots of big earners work in the city but do not ultimately live in the city (Indian Hill, Woodley, Kenilworth, Lake Forest, Hinsdale) but we are talking about Chicago real estate, so the 5,500 number is relevant.

Where do all the other buyers come from? Having lived here for a long time, I think I have part of the answer. There is a tremendous amount of family money in Chicago that enables people (who would otherwise seem of ordinary means) to buy expensive places. And, it’s hard to tell if someone takes out a big mortgage whether they are stretched or if they have cash or marketable securities elsewhere. Some of the firms that run family wealth groups in town provide mortgages that are double collateralized against both the house and their private wealth account (stocks, bonds, funds, etc). You can get a pretty big advance rate with a very attractive spread to LIBOR from the likes of Northern Trust, Mesirow, etc. More than a few LP mansions have been financed this way. I guess my point is current income is only part of the story. Lots of family wealth and trust funds running around — even smaller ones that still allow for some decent purchasing power.

HD,

“Before you know it a majority of those who buy in the upper end are using IO’s driving home prices higher and higher, and the sellers count on market appreciation (and innovative loan qualification standards) for equity rather than the good old time honored principal repayment”

thank you thank you thank you. i have been saying this for a few years in a non comprehensive idiot way with not factual basis to back up. back in 2002 i never understood how some friends and coworker would buy these insane houses when i started home shopping again in 2007 i learned the all to easy IO and why those friends and coworkers had insane places at insane prices. add that to the no doc loans (learned in 2007 also) how everyone and there momma could buy a house and did which made supply low and prices INFLATE. so now starter homes are at the 250k level when the chicago median income is like 45k. hmmmmm

“You did nothing to refute or even attempt to refute my point that option ARM recasts are nothing at all like ARM resets. ”

Dude, I was on your case for *months* about the difference–you used to use them interchangeably yourself, and completely ignore my clarification. Now the all powerful Mish has a post about it and you’re acting like the beacon of truth.

“7 million foreclosures”

That includes in default but not “in” foreclosure loans, too, so a huge amount of that doesn’t qualify as true shadow inventory–yet.

“’shadow inventory’ will be sold to “buddies of bankers””

Once commercial lending frees up just a bit, you’ll likely see ex-bank employees forming companies to buy the shadow inventory in bulk at a big discount, with you-scratch-my-back loans (i.e. Citi lends to buy BofA REO, BofA lends to buy Citi REO). Especially wherever they can buy all (or nearly all) of a condo building.

“so now starter homes are at the 250k level when the chicago median income is like 45k. hmmmmm”

Wait for the detractors to say “oh but the median chicagoer is a renter not a buyer”. Doesn’t change the fact that like 40+% of the city owns, and while a lot of these people may earn more than the median wage, most don’t earn six figures.

But just wait time is on the bears side: the tax credit is slated to expire and the Fed is going to stop MBS purchases by the end of 1Q 2010, which will cause rates to go up and prices to slide further.

Only reason a one bedroom, one bath 800ft condo costs 200-250k in Chicago is all of these government programs to inflate housing. But populist resentment is going to push the government out of housing more and more as time goes on watch and see.

Err the Fed to stop quantitative easing by 3/31/10.

“starter homes are at the 250k level when the chicago median income is like 45k.”

But the median Chicagoan is a renter and the median homeowner didn’t buy their first home in the last ten years. Fun! with stats!

“Wait for the detractors to say “oh but the median chicagoer is a renter not a buyer”. Doesn’t change the fact that like 40+% of the city owns, and while a lot of these people may earn more than the median wage, most don’t earn six figures.”

You got me Bob, but (1) I’m not a “detractor”, (2) it just shows how pointless median of x v median of y is, and (3) I brought up that there are too many high-priced places for the number of “qualified” buyers”.

And it’s still the right point to make if the median sale price drops to anything like detroit levels–median house price in such a disparate market as the city of Chicago is as pointless as the median household income; both are skewed by huge numbers on the south and west sides that simply are not relevant to most of these properties, other than the potential effect on (1) crime and (2) tax rates.

I’m sure some big law partners clear a mil and some clear much less. Rainmakers probably make much more and the service partners probably earn less. Income partners as opposed to equity partners make even less than that and are paid on par with senior associates.

I agree with you there is family money, and there is lots of it, but when you see it all around you it jades your thinking. I spent 8 years of my life at T2 private urban colleges and my god you would think that everyone but you has got a trust fund. But then when I stepped on to the el platform and looked around I quickly remembered that Loyola was only a few thousand kids and Roger’s Park was 100,000 and very few of either cohort had trust funds to buy them real estate. Believe me, I know exactly what your talking about. I have friends who recieved a wedding gift of $250k or $300k and turned around and leveraged that into a million dollar home, they just happened to be good friends, but i’m sure that’s just one of many people in and around social circle that are sitting on some good family money.

“I’m sure some big law partners clear a mil”

And 75% of them live in Hinsdale, Highland Park, New Trier, etc., mostly in houses they bought a while ago, at least til the kids are all out of the house. And “some” clear well over $5 mil (yes, really, but that’s a v. small number).

There are a few hundred that have made over $1mm/year the last few years, fewer this year will and probably even fewer next year. But in any case, it ain’t the biglaw partners that are setting the market for anything around Chicago.

Agree the biggest earners are more likely to have bought their KW spreads in 1986 when they too were up and coming whippersnappers. But like anything it’s a combination of factors. There are quite a few 250-500k income earners in and around the friendly confines of the North side between lawyers, doctors, McKinsey/Bain/BCG consultants, dual-income corporate MBA types, etc. Throw in the family money, increased interest in living in the city and low interest rates and you have a market for overpriced RE. And lest we forget about family business owners. And of course we have the traders.

Bottom line, a 4k a year mortgage is no sweat for a couple with 250k combined base and upwards of 50% more coming in in the form of a bonus in any decent year. That is the starting salary profile for any newly minted MBA/JD/MD couple that finds employment nowadays.

However, if one of them gets laid off…

“a 4k a year mortgage”

Where do I get one? Can I still sign up? Tell me that didn’t expire today.

(hehe)

“upwards of 50% more coming in in the form of a bonus … is the starting salary profile ”

You know very different lawyers than I do. Even in **great** years, it’s 30%, and this ain’t even close to a great year. Most shops, the bonus is going to be the chance to keep working.

Month.

50% is more of a blended statistic. Point is two HOH professional salaries *quickly* add to 300k.

Lawyers have a different comp structure, but the outcome is the same. Hell, they were starting first year associates at 160k not like a year or so ago.

You guys are totally correct. There are plenty of people who can afford $4k a month, but there are far too many homes priced at $4k a month than there are buyers. And furthermore, during the boom, the $4k a month buyers opted to increase their leverage to the max with the IO 5% to 10% down, which means they got more home for their monthly payment.

My household fits into the $4k a month under the traditional gross income guidelines of 36% (no other debt but student loans) but I couldn’t fathom paying that much and keep the lifestyle I have and save for the future. I’m not the highest paid couple I know, by far, and most of them haven’t taken on the $4k a month mortgage either. that’s a nice market, and let me tell you, I highly doubt in the furture that will include 3 bedroom townhomes in bucktown across the street from teh el tracks.

it’s a niche market i meant to say..

“Bottom line, a 4k a year mortgage is no sweat for a couple with 250k combined base and upwards of 50% more coming in in the form of a bonus in any decent year. That is the starting salary profile for any newly minted MBA/JD/MD couple that finds employment nowadays.”

First, there are literally no jobs for newly minted MBAs, second, they (us) don’t make that much money anymore. I had interview last week for internal audit position at pretty large company and the starting salary is only S44K (benefits are good, but still)! Even Big4 starting salary for recent grads with Master’s is about $60K – and they are not hiring anyway.

While the discussion of how many people make $250,000 a year combined salary is interesting (yet again- as every few months we have this conversation), I have an off topic question of homedelete and anyone else who may know:

If someone wants to do a short sale (the home is not yet on the market)- what is the procedure? Do they contact a real estate agent first and list it or do they hire a real estate attorney to help manage the process?

Thanks!

By the way- I happen to know plenty of lawyers and many of those biglaw associates who were making $250,000 a year are now out of jobs (some for as long as a year- with no hope of employment in sight.) It sucks right now.

short sales: i’ve never actually done one, I try to stay away from them personally because they take so long; but from what I know about them, you first hire a realtor, preferably one with short sale experience, who has an attorney who also has the time. Then, either the lawyer or the realtor submits paperwork to the bank and then you wait, wait, wait for the bank to approve the short sale. takes months. and the bank 50% of the time makes you sign a prom note for the deficiency. Lots of calling the bank, lots of waiting. When you get approved (if you get approved) they tell you the terms of the deal with little or any room for negotiation. Any bargaining takes even more time. Then as the seller you sign the package and on closing day the bank takes a short sale pay off and releases the lien.

Thanks Homedelete. I thought you might have some experience with them. But this is basically what I thought the procedure was.

If you are buying a short sale, the process is like any other purchase except that it may take forever and a day. In many cases, the short sale is not already approved by the bank so the process gets dragged out waiting on the mortgage holder to approve the short sale offer.

If you are listing a property and need to sell short, most banks have a process that the seller has to go through to show hardship I believe.

312: This is why it generally only pays to go to Top 15 or so mba/law schools.

“There are plenty of people who can afford $4k a month, but there are far too many homes priced at $4k a month than there are buyers. ”

HD: See, we agree about something–I said that upthread.

“312: This is why it generally only pays to go to Top 15 or so mba/law schools.”

Is that why the number of employers showing up at Harvard Law School this fall is down 50%?

Hundreds of Harvard Law School grads will likely not have jobs when they graduate next spring (and the spring after that.) Now, I concur, that their odds of eventually finding something that pays decently are better than those who graduate from a fourth tier school. Of course.

But the pain is everywhere.

The lawyers I know out of work for a year DID go to top ten law schools. There are, unfortunately, simply thousands of them out of work right now- all with the same credentials. And those high paying jobs aren’t coming back.

“Hundreds of Harvard Law School grads will likely not have jobs when they graduate next spring (and the spring after that.)”

Do you really think that the “employed at graduation” stat at HLS will be below 60% this year? Really?

I agree that a much higher than normal % of them will have $20k state court clerkships and NGO jobs and not be making enough to service their debt, but I would wager that HLS gets their employment number over 90% (ie, less than 50 unemployed) one way or another. In part, the HLS grads will displace grads from lower-ranked schools in a cascade effect, leaving median students at 4th tier schools really out of luck.

Sabrina: # of employers showing up versus students employed are two entirely different things. The job offers are there and the students are still making big bucks. Typical consulting offer at Kellogg & Chicago GSB is $125k-$130k with a $25 to $40k signing bonus. All the big feeder companys are still sending hordes of recruiters to wine and dine. Brand management is around $100k. Biglaw offers are up to $160k. I-banks are still hiring. Management rotation jobs at f500 are around $100k. McKinsey probably hires close to 100 people from HBS alone out of a class of 800.

Anon is correct. What happens in markets like these is that the big feeder employers continue to hire however they scale back going to lower tier schools since the top tier students generally aren’t as picky in this type of economy.

Most grads at those schools who don’t have jobs is usually by choice because they are looking for something special that falls outside of the normal recruiting process so they have to get it on their own hustle and it may be right at graduation before they find what they want.

I assure you, no one at those schools are freaking out that they can’t get a job. It is all relative, they are freaking out maybe because they have to settle for Accenture instead of McKinsey or go to JP Morgan instead of Blackstone. Instead of consulting, it is brand management. However, they all are still making six figures.

“However, they all are still making six figures.”

And if you believe the official employment stats from these schools I’ve got a bridge to sell you.

No doubt there is a lowering of expectations and new grads are opening up to new fields, but there is a huge degree of massaging those stats. Those stats are the best marketing tool these top schools have and if you believe the school just collects and presents the data instead of actively managing it I’ve got a unicorn to sell you along with that bridge.

“no one at those schools are freaking out that they can’t get a job.”

Well, at the law schools, I think there is some freaking out, but (1) they’re law students, so the freak-out factor is high and (2) Harvard/Yale/Stanford student will have a very different experience of it from non-top students at G’town/Cornell/whatever.

It’s similar at the b-schools, with the non-top students at the non-top 5 schools having higher anxiety than folks at HBS/Stanford/UC-NW-Penn-depending-on-field.

Bob:

I am not looking at “stats”, I see the actual offer letters every year from handling the financing on dozens of home purchases of new business/law grads from top schools in Chicago and other major cities. The stats are accurate.

“The stats are accurate.”

No russ you see a sample size, which is preselected. You have no way of knowing. Having been there myself, I knew a broad swath of my class and those without offer letters weren’t actively hounded down by those keeping the stats.

Not saying there aren’t newly minted MBAs with coin from these schools, but remember the FT class sizes are around 600 people. Thats 1,200 total. If you’re literally doing dozens of deals for the subset that is able and willing to buy you must be the most active mortgage broker in recent history.

“I am not looking at “stats””

“The stats are accurate.”

Also russ if you aren’t looking at “stats” how can you make a statement that they are accurate? 😀

“Sabrina: # of employers showing up versus students employed are two entirely different things. The job offers are there and the students are still making big bucks. Typical consulting offer at Kellogg & Chicago GSB is $125k-$130k with a $25 to $40k signing bonus. All the big feeder companys are still sending hordes of recruiters to wine and dine. Brand management is around $100k. Biglaw offers are up to $160k. I-banks are still hiring. Management rotation jobs at f500 are around $100k. McKinsey probably hires close to 100 people from HBS alone out of a class of 800.”

Russ is dead on. I know because we are hiring them (and competing like hell with McKinsey for each one). Everyone is more selective and there are fewer jobs to go around, but the best and brightest (from the best schools) still get paid (as they should be). Chicago, because of its two excellent schools (NWU and UC), pumps out a lot of these guys. Even investment banks are hiring, as Russ notes, but now for restructuring advisory instead of MBS desks.

Sabrina, to your point, a lot of the lawyers that are out of work did securitization work. That is understandable. Many others worked in corporate securities deals, also understandble. But, I dont know many IP attorneys or labor lawyers that are out of work right now. And the bankruptcy guys — forget about it.

Ok I know this is “Chicago” real estate discussion, but can we for a second comment on this doozy — it’s too good not to post.

http://www.chicagobreakingnews.com/2009/03/arrest-made-is-winnetka-drug-bust.html

http://www.redfin.com/IL/Winnetka/384-Hawthorn-Ln-60093/home/18954828

Same house just now listed for a 50% discount. Question for the group is did the drug bust precipitate the foreclosure or did the foreclosure lead junior into a life of crime. In East Winnetka of all places. Next to a school!

I-banks might be hiring newly minted grads because they are firing 300k/year associates. It still doesn’t bode well for a different segment of the real estate market.

A lot of big i-bank recruiters have really scaled back as well: Lehman, Bear and Merrill no longer exist. Aside from GS, DB and CS, I’d be willing to bet hiring is down at the remaining i-banks. Hedge funds? The industry is going through its biggest downsizing in its history.

There is a reason people fight tooth and nail to go those schools and this is the main one. Employment opportunities – even in a down market. Like I said, everyone may not be getting their “dream job” at Google or finding a job in NYC or their first choice city, but they are getting jobs and those jobs pay well. I am a grad of one of those schools and also did quite a bit of recruiting at those schools as well when I was working at a consulting firm. I also saw how the recruiting situation changed when the bottom fell out of the market in ’01-’02 when the dotcom bubble burst when large numbers of student got their offers rescinded. They still found other jobs.

Yes, I am one of the higher producing mortgage brokers and most of my clients are in that “niche.”

Russ — off topic (whatever that topic is) but have you ever done a deal where buyer utilized an Illinois land trust and the lender was ok with that?

It depends on the lender as all of them have specific guidelines as to how they handle trusts. Typically, a land trust is ok. No lender that I am aware of will lend to an irrevocable trust though. Here are the guidelines from a major lender in regards to land trust.

“A review of the trust agreement by the Correspondent or their counsel must ensure:

• the trustee is an institution, and

• at least one borrower is a beneficiary of the trust.

Additionally:

• a letter from the institutional trustee must certify lender will be notified if the trust attempts to change names,

• the note must be signed by the borrower only, and

• the security instrument must be signed by the trust only.”

HBS publishes these stats – http://www.hbs.edu/recruiting/mba/resources/career.html

“a deal where buyer utilized an Illinois land trust and the lender was ok with that?”

In addition to what Russ sez, I can’t imagine that any bank in Illinois would have any issue with it, if you were using either that bank or a major title company act as the trustee. I’d take issue if you were using the Bank of Hooterville or Bob’s Land Title as the trustee.

“312: This is why it generally only pays to go to Top 15 or so mba/law schools.”

Working 80 hours/week is not for everyone, even if it pays well:). I’m happy with my my MBA from “T2 private urban college”, especially considering I didn’t have to pay for it.

Of course top students from top school making enough money (even when economy is bad) to afford Chicago real estate at inflated prices but how many of them are actually buying right now?

Why is everyone focused on MBAs and JDs, don’t you know how many traders there are in Chicago with major bank?