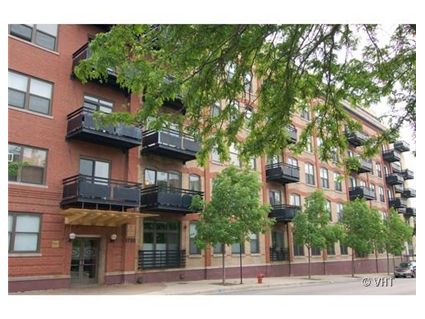

Still Trying to Sell: 1735 W. Diversey in Lincoln Park

We chattered about a foreclosure in 1735 W. Diversey in Lincoln Park in November 2007.

The foreclosure was a two bedroom, two bath penthouse unit.

Unit #608: 2 bedrooms, 2 baths

- Sold in October 2000 for $206,500

- Sold in May 2003 for $314,900

- Foreclosure auction price of $504,725 in November 2007

- Has not yet come back on the market

We also chattered about another penthouse unit that was on the market. It had a 90 foot wrap-around deck.

It is still available and has been reduced.

Unit #615: 3 bedrooms, 2 baths, 1715 square feet

- Sold in June 2000 for $368,000

- Sold in April 2002 for $395,000

- Sold in July 2006 for $492,000

- Listed for $530,900 in the fall of 2007

- Reduced

- Listed in November 2007 for $515,900

- Reduced

- Currently listed for $490,000 plus $20,000 for parking

- Taxes of $7215

- Assessments of $490 a month

- Koenig & Strey has the listing

These people are humorous. Do they really expect to sell it at auction for nearly 70% more than the 2003 price?

This should be a 2002 rollback. These are very mundane apartments. Other, better, units in Lincolm Park are languishing at more attractive prices.

The foreclosure is even funnier. Not only did someone not clue them in that NINA loans might not be a good idea for the future of their company, but also apparently they forgot to get clued in that theres no way this will auction for 500k.

At least it will generate some laughter from the audience during the auction.

So, the 2br 2 ba hasn’t sold? Is it still owned by the bank?

The 2br 2 ba did sell, on 6/24/08

trains used to turn around in the backyard of that place back in 2001. it was pretty cool but (from google maps) it looks like they have taken the tracks out.

Here is the history of unit 608 from ccrd (all included parking):

10/27/00 puch from developer for $283,000

3/25/03 sold for $316,000 with $319,000 mortgage.

5/16/03 2nd mort for $40,000

10/22/03 2 existing mortgs refied for $70,000 & $322,500

11/05 Lis pendens filed on both mortgages

8/21/06 sale-vation from a buyer at $475,000

8/21/06 actually, HSBC Mtge was the savior with 100% loan

2/18/08 deeded to HSBC Mtge

5/23/08 sold by HSBC Mtge for $315,000

5/23/08 mortgage from JPMorgan Chase for $283,500 (90%)

Given how early we are in the foreclosure tsunami, the recent buyer of the REO is most likely still catching a falling knife.

Hmm — looks like 608 (the foreclosure) has sold.

MERS transferred the property to HSBC on June 06, 2007.

HSBC keep the property through the auction, formally receiving the deed on Feb 18, 2008.

HSBC then sold (warranty deed) to an individual on May 23, 2008 (recorded 06/24/2008) for $315,000.

The individual got a 90% mortgage from JPMorgan Chase. One parking space was included.

[I’m also seeing slightly different previous sale data:

10/27/2000 sold for $283,000

03/25/2003 sold for $316,000

08/21/2006 sold for $475,000

The association filed two liens against the 2003 buyer and one against the 2006 buyer. Two banks filed lis pendens against the 2003 buyer in late 2005 (JPMorgan Chase second followed by ABN AMRO first). The property did not transfer until the 2006 sale, however.]

All data pulled from CCRD.

Question: what happens to the association’s lien ($3834) against the foreclosed owner now? Should they have gotten any money at some point in the foreclosure cycle, or is the association permanently out that money (plus legal fees)?

For those who are wondering why G and I report a different sale date from Jason, G and I reported the “executed” date from the recorder of deeds; Jason reported the “recorded” date which is reported by the recorded (and many other sources).

It is a fair question why it takes Cook County a month to process the paperwork.

The association’s lien is worthless. (To make a long story short.) The foreclosure extinguishes it. However, Illinois Passed a new law effective in March that the BUYER of a foreclosed property is responsible for the last 6 months of Association dues from the date of sale. he bank would be responsible for any months it owned the property prior to the sale.

Another BS law to help banks out and screw normal people if you ask me.

If someone were to challenge that Illinois law in court theres a good chance it would be overturned. Its ridiculous to try to levy a liability on someone for activity that occured prior to them taking ownership of a place.

I agree. I am still trying to find the citation, its buried somewhere.

Found it:

(4) The purchaser of a condominium unit at a judicial

foreclosure sale, other than a mortgagee, who takes possession of a condominium unit pursuant to a court order or a purchaser who acquires title from a mortgagee shall have the duty to pay the proportionate share, if any, of the common expenses for the unit which would have become due in the absence of any assessment acceleration during the 6 months immediately preceding institution of an action to enforce the collection of assessments, and which remain unpaid by the owner during whose possession the assessments accrued. If the outstanding assessments are paid at any time during any action to enforce the collection of assessments, the purchaser shall have no obligation to pay any assessments which accrued before he or she acquired title.

Wow, I ama lawyer and that is still confusing.

I am somewhat familiar with California law, which provides that the priority for liens is: property taxes, up to six months of assessments, first mortgage, other regular assessments and special assessments, other liens.

It sounds like Illinois may be trying to mimic that law.

If the law forces an assessment lien to be dealt with in escrow, it seems almost acceptable. If it allows the lien to survive the issuance of a new deed, that does seem ridiculous.

This area of diversey is crammed with traffic all the time, not close to public transportation..and not that clo

The IL law is clearly different from the CA law.

And it looks bizarre. If I’m piecing it together correctly it goes something like this: *If* the association filed a lien against the deadbeat owner (“institution of an action …”) they may collect unpaid assessments for the six months prior to that lien from the new owner, whether the new owner bought at the foreclosure auction or later bought from the deadbeat’s lender.

Bob,

Such a requirement on the buyer would simply be factored into the purchase price (or should be, if the buyer is smart), thereby reducing the amount the bank gets for the property.

But yeah, I don’t see many reasons why banks should get any pass whatsoever at any time on paying assessments due while they are in possession of a property.

It’s better for the buyer to take responsibility for the assessment arrears than to put it on the other owners in the building. The buyer can just adjust the price accordingly.

However, if the condo association cannot recover those assessments, they fall upon the innocent- other owners in the building. This potential liability makes condo ownership a very scary proposition. We are talking about potentially very large liabilities that other owners did nothing to incur, particularly if they bought into a new development before a condo association was in place.

If the previous foreclosed owner cannot pay, which is usually the case, then the liability should transfer to the next owner, in this case the foreclosing lender.

NO WAY! Sorry, but the condo ass’c bites it.

I see Laura’s point and now the point of the law, however unfair to the individual. Without this law this could have a crippling domino effect on buildings with a lot of foreclosures and basically shut down the condo market for smaller buildings entirely.

At least this way the owner can negotiate with the bank to catch a price break if they are smart (if they aren’t they deserve the tax). Otherwise we’re in a situation of rapidly declining prices due to more foreclosures in the building and rapidly escalating HOA dues, a spiral deathtrap of foreclosures->higher HOA dues for regular owners->lower property prices due to higher HOA dues->more foreclosures.

I don’t consider the law unfair to the individual, who is free to walk away from the deal if the price isn’t dropped in keeping with the assessments and/or taxes due on the unit.

I have looked at a couple of units in foreclosure, and in both cases, the price had been dropped to offset the assessments in arrears. Usually, the price has to be dropped more, because the buyer has to come in with the cash to pay those assessments.

It’s the only way to keep the entire association from taking the hit. As it is, many condo owners who bought honestly and within their means are staggering under the load of utility bills and upkeep way beyond what they contracted for when they bought into the place. Many are being pushed into insolvency because of this, and many others are working the desk and mowing the lawn in high rise buildings with half the hall lights turned out, because of numerous units in default in the building.

As it is, the association will have to wait long enough for the money to place a pretty heavy burden on the other owners.

I love apartment life and condos, but this situation, which is now so commonplace because of the massive number of unsold units and defaulting buyers AND developers, is making me wonder if I should buy a condo at all.

I’m certainly interested only in buying into a stable association of long standing, with board approval required for buyers. Now that you have to have a sizable down payment no matter where you buy, co-ops are looking better every day, because they make sure buyers are financially qualified to own.