Crain’s reports on homesellers who have already moved into a new property and haven’t been able to sell the first.

They are paying two mortgage payments- sometimes for months.

Ryan and Lynda Hamilton aren’t sweating the five months of construction delays slowing completion of their $690,000, 3,900-square-foot home in Elgin. They have bigger problems. Namely, their 2,700-square-foot, single-family home in the Old Irving Park neighborhood, which has languished on the market since May 2007, leaving them carrying two sizable mortgages.

“I thought for sure it would sell in two or three months,” says Ms. Hamilton, 39, regional director in Chicago with HelmsBriscoe Inc., an international meeting-site procurement company. She and her husband, Ryan Hamilton, 35, owner of Chicago-based software developer Bluebuzzard Technology Group Inc., originally listed the four-bedroom, 3.1-bath home for just $640,000 — which they viewed as a deal for a potential buyer. They had watched homes on their street sell for closer to $700,000 within a few months of listing.

But those were different times.

The couple has now dropped the price twice, first to $619,000 and recently to $599,000, upon the advice of their real estate agent, Cindy Risch of the Lincoln Park office of @properties Inc. “She said it would bring in more traffic,” Ms. Hamilton explains.

It didn’t.

“I just lost another $20,000 for nothing,” she adds. “We’ve shown it once in the last two months.”

Now faced with paying their old mortgage, new mortgage and a home-equity loan they used to buy their lot, the Hamiltons, who have three daughters, are trying to find a renter with an interest in buying. This, they say, was a worst-case scenario.

“We definitely needed the equity in the home,” says Ms. Hamilton. Renting, she adds, won’t cover all their home-related expenses.

But they weighed the alternatives — dipping into their children’s education fund, borrowing against their retirement accounts, taking out a bridge loan — and found them even less attractive. Ms. Hamilton knows the family can’t hold on financially for another eight months. “There’s only a certain amount of time that we can pay all three,” she says. “Our savings are only so thick.”

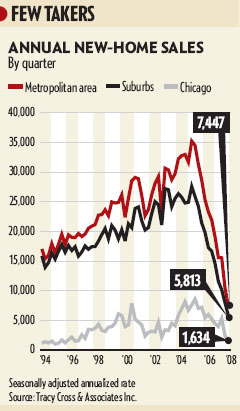

Several sellers are trying to sell condos in a market with a ton of inventory. The average time buyers live in a downtown loft is two years. As all the professionals decide to move to other cities or have other lifestyle changes (marriage, children etc.) they are finding its not so easy to just pick up and move in this type of housing market.

Renting out condos isn’t really much of an option. As we’ve chattered about, the rents aren’t covering the costs of ownership.

Eric Fontaine, 37, and Colleen Borkowski, 28, are eager to begin their new life together in Boston, where Mr. Fontaine relocated last fall to take a product marketing management position with Setra Systems Inc., a manufacturer and designer of pressure measurement instrumentation in suburban Boxborough. The couple is getting married on May 3 in South Bend, Ind., but their dream home is on hold.

That’s because when they moved, each still owned a condo in Chicago.

“My hopes were high, but when the market info started coming in, that started making me a little more skeptical,” says Mr. Fontaine, who placed his 2001 two-bedroom, two-bathroom condo in east Ukrainian Village on the market with Prudential Preferred Properties in September. He dropped his asking price to $359,000 — $30,000 less than the original asking price — and at press time had found a buyer after six months of carrying the mortgage.

His fiancée’s condo, built in 2005 and fully upgraded, is situated among a glut of newer construction in the Lincoln Square neighborhood. Ms. Borkowski put it on the market in November with Keller Williams Lincoln Park and “would love for somebody to like it as much as I did.”

“To know that nobody else wants it is hard,” she says.

Ms. Borkowski, a paralegal with law firm Wilmer Hale’s Boston office, has already lowered the price once, from $375,000 to $369,900.

While the couple debated renting out one of the places, they have no desire to be long-distance landlords.

“The tough part is you can’t really do both,” Mr. Fontaine says. “You have to make a choice. If you do rent it, you can’t sell it. For us, we’d rather just get out from under it.” Plus, Mr. Fontaine doubted rental income would cover either property’s mortgage, property taxes and assessment.

How long can these sellers hold on?

We’ll know by the end of this summer. As one seller of a Bucktown townhouse said:

“We still have quite a bit of equity,” he says. “It’s something we can withstand a couple of months. I’m hoping I don’t have to see where things are at come August and September.”

Stuck With Two Mortgages [Crain’s]